Table of content

The Question Every Advisor Asks: "What Would I Actually Make as an Independent?"

Lane had spent years working in operations at a large brokerage firm and described challenges common across many traditional financial services environments. As he described in a recent interview: "I was 23 years old...I worked my butt off and I had no support. And so it was very challenging...and I felt that the environment was challenging."

He wasn't alone. Many advisors across wirehouses, insurance companies, and broker-dealers face the same question: What would my income actually look like if I went independent?

The answer varies widely based on advisor circumstances — but it's clearer than most advisors think.

If you've ever wondered about independent financial advisor income, you're asking the right question. This comprehensive analysis reveals what independent advisors actually make, using verified advisor stories, documented compensation structures, and honest comparisons across business models.

Understanding Independent Financial Advisor Income: What Really Matters

What Does "Independent Financial Advisor Income" Actually Mean?

When we discuss independent financial advisor income, we're referring to advisors who:

● Own their practices (vs. being employees)

● Have autonomy over client service decisions (vs. following firm mandates)

● Build equity value (vs. building zero)

● Control compensation structures (vs. accepting corporate grids)

This includes:

● RIA advisors (solo practices or firm-affiliated)

● IBD-affiliated advisors (independent contractors)

● Hybrid RIA advisors (RIA ownership with firm support)

The Four Factors That Determine Independent Advisor Income

Independent financial advisor income depends on four critical factors:

1. Business Model Your choice between solo RIA, IBD-affiliated, or hybrid RIA dramatically impacts both gross revenue and net take-home.

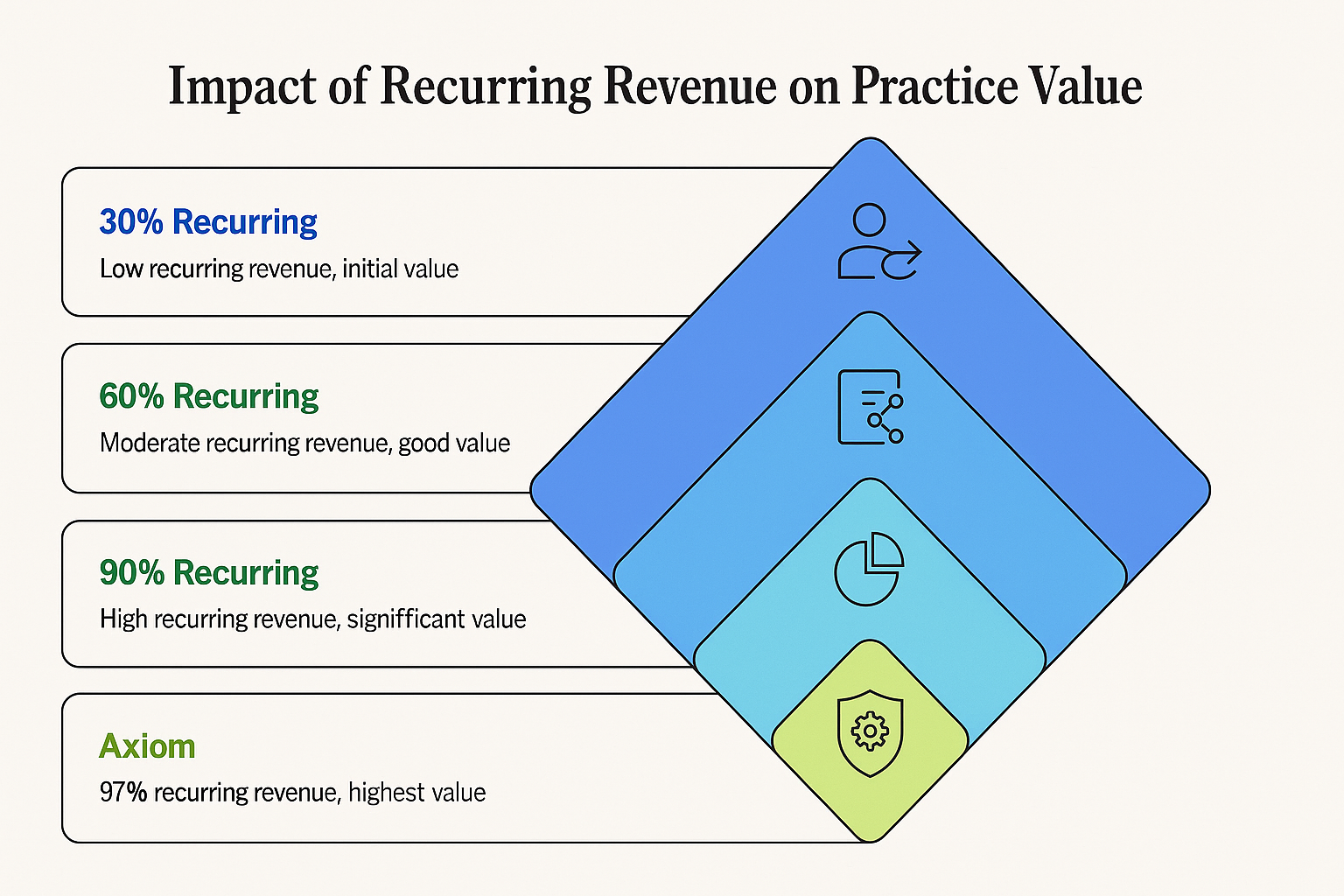

2. Recurring Revenue Percentage The percentage of your income that's recurring (vs. transactional) affects both stability and practice valuation. Recurring revenue industry averages (30-35%)based on commonly referenced industry research; illustrative only. According to internal interviews and project research files, some advisors at Axiom reported approximately 97% recurring revenue across their advisor network. This may not reflect typical results.

3. Production Level Your total production (revenue generated) serves as the baseline, but what matters more is what you keep after expenses.

4. Operational Efficiency The time and money spent on operations (vs. client service) directly impacts both income and quality of life.

Business Model Comparison: Understanding Your Options

Different business models create vastly different economic outcomes. Here's an honest comparison:

Wirehouse Model

Structure:

● Grid-based payout system

● Multiple deductions and adjustments

● No equity ownership

● Limited autonomy

Economics:

● Gross payouts typically range from 40-70% depending on production

● Various deductions reduce net take-home

● Zero equity building

● Income includes base salary or draw in some cases

Reality: Some advisors often discover their "60% grid" may become 40-45% effective payout after all deductions, adjustments, and fees.

Independent Broker-Dealer (IBD) Model

Structure:

● Higher payout than wirehouses

● Advisor pays for own infrastructure

● Some equity building potential

● More autonomy than wirehouses

Economics:

● Gross payouts typically 80-90%

● Advisor responsible for technology, compliance, staff

● Can build equity value (typically 2.0-2.5x revenue)

● More operational burden than wirehouses

Reality: Better economics than wirehouses, but significant operational time investment required.

Solo RIA Model

Structure:

● Complete independence

● 100% of gross revenue

● Full operational responsibility

● Maximum autonomy

Economics:

● 100% gross payout

● Advisor manages all vendors, compliance, technology

● Can build significant equity value (2.5-3.5x revenue)

● Highest operational burden

Reality: Best for advisors who want complete control and have operational expertise or can afford to hire it.

Hybrid RIA Model (Axiom's Approach)

Structure:

● RIA ownership with comprehensive support

● High payout with operational assistance

● Equity building with reduced burden

● Autonomy within framework

Economics:

● Based on internal interviews, Axiom advisors may receive around 95% payout, depending on individual agreements.

● Comprehensive back-office services provided

● Equity building with higher valuations due to recurring revenue model

● Minimal operational time investment

Reality: Designed for advisors who want independence economics without operational overwhelm.

Not sure which independence model fits YOUR practice? Each model creates different economic outcomes. Take our 2-minute assessment to find out which structure aligns with your goals and situation.

The Numbers Nobody Discusses: Recurring Revenue's Impact

Here's what most independent financial advisor income analyses completely miss: recurring revenue percentage is the single biggest factor affecting both income stability and practice value.

Industry Context: The 32% Problem

According to Axiom leadership interviews, the broader financial services industry averages approximately 32% recurring revenue. Most advisors operate with mixed compensation:

● 32% recurring fees (advisory)

● 68% transactional (commissions, one-time fees)

This creates:

● Unpredictable monthly income

● Constant pressure to sell

● Lower practice valuations

● Conflicts of interest

Figures based on internal Axiom interviews referencing national averages; illustrative only.

Axiom's Model: 97% Recurring Revenue

As stated by Axiom's founder in a recorded interview: "Ours is 97 percent recurring. We have people not eating the seeds. They're not taking the upfront option...nationally with our current broker-dealer, we're 97 percent recurring, 32 percent recurring for the country."

This fundamental difference creates:

Transactional Model (Industry Average~32% recurring):

● High month-to-month income variance (±25%)

● Must constantly generate new business

● Commission-driven client conflicts

● Lower practice valuations

● High stress and burnout

Recurring Model (Axiom ~97%recurring):

● Minimal income variance (±3%)

● Growth compounds over time

● Aligned interests with clients

● Higher practice valuations

● Sustainable business model

Why Recurring Revenue Matters for Practice Valuation

Practices are valued based on the predictability and sustainability of their cash flow. Higher recurring revenue creates:

● More attractive businesses to buyers

● Higher valuation multiples

● Easier succession planning

● Better financing options

● Greater business stability

While specific valuation multiples vary based on many factors, the principle is clear: predictable recurring revenue creates more valuable businesses.

Real Advisor Stories: Verified Transitions

Bryan's Story: From Product Pressure to Professional Pride

Bryan spent 10 years at a large national financial firm before transitioning to Axiom in March 2020. Here's his actual experience, from a recorded interview:

Before Transition (- 10 years):

"My income was about a hundred thousand dollars. And after 10 years...first of all, I felt like I was failing as an advisor because I wasn't hitting enough income for where I should be. I felt like a hypocrite as well, because in order to get that level of time in the business, I had to go into quite a bit of debt just to be able to keep myself afloat."

Bryan described the ethical conflicts: "I just did not want to feel like I was having to push products to make money. I always felt like, to be a good financial advisor, you should be able to give people the best advice for their situation and not have to really worry about how you were compensated."

On the culture: "Here I was... 36 at the time... I didn't feel like I fit the environment. They train you really well, but they also have a reputation for pestering the snot out of everybody. I just didn't want to be looked at like a used car salesman."

After Transition (Axiom):

"This has been the best career move that I could have made...I never took a cut in income...last year my revenue was right at 300,000 versus just four short years ago, it was 130 [thousand]."

On the business model difference: "It's a drastic difference. And the thing is, is it's not because I'm selling people stuff they don't need. I'm helping people and because I'm helping people, more people are coming to me."

On client service: "Truly I am giving people advice to better their situation. As a part of fee based planning, we don't just...we still do investments and we still do insurances, but that's just pieces of the puzzle. I'm giving people advice around every aspect of their finances."

On quality of life: "My sleep now compared to then? Oh man, it's night and day."

On referrals: Bryan reported receiving more referrals after transitioning, which he attributed to the client outcome she was delivering. This was his personal experience and is not typical or guaranteed.

Bryan’s Reported Outcomes (Verified Interview, 2024):

● Revenue grew from ~$130,000 to $300,000+ over 4 years

● He reported improved work-life balance and a more fulfilling practice model

● Emphasized transition from product-driven sales to comprehensive client planning

● Described this change as the best move of his career

● Reported increased referrals driven by client outcomes, not sales tactics

This individual's experience is based on their specific circumstances and does not represent typical results. Individual outcomes vary significantly based on production, expenses, client retention, and operational efficiency.

Wondering how YOUR income would translate to independence? In Bryan's individual case, his reported income increased over four years. While results vary, discover what independence could look like for your specific situation with our free income comparison calculator.

Lane's Story: From Operations to Building a Support System

Lane worked in operations at a large brokerage firm before joining Axiom in 2017. While not an advisor himself, Lane now manages Axiom's advisor services department and has unique insight into both sides.

On His Experience:

"I was 23 years old...I worked my butt off and I had no support. And so it was very challenging...the culture was extremely poor. I was actually looking to leave the industry."

On What Makes Axiom Different:

"Jerry’s leadership is very involved and values-driven. That makes a huge difference to the kind of support we provide advisors. He gives a lot back to the advisors. We offer a lot of support."

On Transition Support:

"We will work with the new recruits. So if a guy decides to join and commit, we'll work with him for the first six months and move over his entire investment book from their previous firm...it's a big decision. They're business owners, moving all of their clients to a new company. And so handling that with care is very important and we will work with them for the first six months at no cost."

On Advisor Pain Points:

When asked about emotional challenges advisors face, Lane identified three key areas:

- Support: "The lack of support that the agency actually offers. So a lot is on the advisor. They're paying out of pocket for an assistant. They're paying out of pocket for a junior advisor. They're paying out of pocket for business acquisition."

- Culture: The competitive, pressure-driven environment at traditional firms

- Freedom: "I don't think they're able to actually practice as a business owner. From my perspective, they don't have that freedom like they do here under Axiom."

Individual experiences vary and are not guarantees of results for other advisors.

Compensation Models Explained: How Independent Advisors Get Paid

Understanding compensation models is essential to evaluating independent financial advisor income:

Advisory Fee Model (Recurring Revenue)

How it works: Advisors charge an ongoing percentage of assets under management (commonly 0.50-1.50% annually), creating predictable recurring revenue.

Billing: Typically quarterly for ongoing service relationships

Pros:

● Predictable income

● Aligned with clients (grow together)

● No sales pressure

● Sustainable long-term model

● Higher practice valuations

Cons:

● Market-dependent (revenue drops if markets fall)

● Requires significant AUM to support practice

● May not fit all client types

Recurring Revenue: 100%

Retainer/Subscription Model

How it works: Fixed monthly or quarterly fees independent of AUM

Pros:

● 100% recurring revenue

● Not market-dependent

● Works for all asset levels

● Clear value exchange

Cons:

● May be harder to scale to high income levels

● Requires clear service definition

Recurring Revenue: 100%

Hourly Model

How it works: Project-based billing with no ongoing relationships

Pros:

● Clear value exchange

● Works for specific situations

Cons:

● 0% recurring revenue

● Unpredictable income

● Low equity value

● Constantly finding new work

Recurring Revenue: 0%

Commission Model

How it works: Transaction-based compensation where advisors are paid when clients buy products

Why Independent Advisors Avoid It:

● Creates conflicts of interest

● Unpredictable income

● Not truly fiduciary

● Lower practice valuations

● Ethical concerns

This is precisely what many advisors are trying to escape when they go independent.

Recurring Revenue: 0-30% (if some ongoing trails)

Axiom’s Reported Compensation Model: 95% Payout and 97% Recurring Revenue (Based on Internal Data)

Axiom's approach combines high payout with comprehensive support and recurring revenue focus:

Payout Structure: 95% payout to advisors (verified from leadership interviews)

What's Included in the 5%:

● Complete technology stack

● Compliance monitoring and support

● E&O insurance

● Operations support

● Marketing infrastructure

● Practice management guidance

Recurring Revenue Focus: 97% average recurring revenue across organization (vs. 32% industry average)

How This Creates Different Economics:

Illustrative Example (Educational Purposes Only):

An advisor with $400,000 in production:

● Gross payout: $380,000 (95%)

● Personal expenses (assistant, marketing): ~$60,000

● Net income: ~$320,000

● Recurring base: ~$370,000 (97% of production)

According to industry averages cited in internal Axiom documentation and leadership interviews, many advisors operate with approximately 30–35% recurring revenue. This means that for a $400,000 production level, approximately $128,000 may be recurring, with the rest derived from transactional or commission-based revenue. Actual results vary.

Note: This is an illustrative example for educational purposes only. Individual results vary significantly based on production, expenses, client retention, and operational efficiency.

Geographic and Experience Considerations

Geographic Income Variations

Independent advisor income varies by geographic market based on:

● Cost of living

● Local competition

● Client wealth levels

● Market sophistication

Advisors should evaluate opportunities based on their specific market conditions and quality of life considerations, not just nominal income figures. Actual income levels vary widely by market, advisor experience, and business structure.

Career Stage Progression

Independent advisor income typically evolves through distinct phases:

Years 1-3: Building Phase

● Focus: Building client base, learning operations, establishing systems

● Challenge: Lower initial income while building recurring base

● Opportunity: Foundation for sustainable growth

Years 4-7: Growth Phase

● Focus: Established client base, referral momentum, scaling operations

● Reality: Income typically accelerates as recurring revenue compounds

● Benefit: More predictable income base

Years 8-15: Mature Phase

● Focus: Strong recurring revenue base, efficient operations, lifestyle balance

● Achievement: Significant income with manageable workload

● Value: Building substantial equity value

Years 15+: Peak Earning Phase

● Focus: Large stable client base, maximum efficiency, significant equity value

● Opportunity: High income with succession planning options

● Legacy: Sellable business asset

Long-Term Wealth Building: The Equity Factor

The primary wealth-building difference between employee advisors and independent advisors is equity value.

Employee Advisor Wealth Building:

● Income only (no equity)

● Zero business value at retirement

● Cannot sell practice

● Deferred compensation often forfeited if leave

Independent Advisor Wealth Building:

● Income plus equity

● Business value typically worth multiples of annual revenue

● Can sell practice at retirement

● Can transition to next generation

Why This Matters:

Two advisors with identical $400,000 annual production over 25 years:

Employee Advisor:

● 25 years of income

● Retirement value: $0 (no business to sell)

● Total wealth: Income only

Independent Advisor:

● 25 years of income (typically higher net)

● Retirement value: $800K - $1.4M+ (business sale)

● Total wealth: Income + equity value

Hypothetically, over a 25 - year career, the equity value of an independent practice may amount to several times annual revenue — potentially resulting in seven-figure valuations. This is for illustrative purposes only and not a guarantee of earnings. Individual results vary significantly.

Why Independent Advisors Often Earn More

Many advisors interviewed for our research reported than employee advisors at comparable production levels due to:

1. Higher Payout Structures

Eliminating multiple layers of corporate overhead means more revenue reaches the advisor.

2. Recurring Revenue Compounds

Unlike starting over each month with commissions, recurring revenue stacks and grows.

3. No Product Conflicts

Ability to recommend best solutions (not just proprietary products) improves client outcomes and drives referrals.

4. More Time for Clients

Less administrative burden means more time for relationship-building and service.

5. Authentic Fiduciary Relationships

True fee-only relationships eliminate sales pressure and build trust, driving organic growth.

As Bryan noted: "Because I'm helping people, more people are coming to me...I'm in front of people now that I wouldn't have been able to be in front of before just because of what I was able to do then versus what I do now."

Applies specifically to fee-only advisors; individual circumstances vary.

FAQ: Independent Financial Advisor Income Questions

Q: How much do independent financial advisors really make?

A: Independent financial advisor income varies widely based on production level, business model, recurring revenue percentage, and operational efficiency. Independent advisors typically retain a higher percentage of their production than employee advisors because they eliminate corporate overhead layers. However, they also bear responsibility for their own expenses.

The key differentiator is equity building: independent advisors build sellable business value (often worth 2-3x+ annual revenue), while employee advisors build zero equity. Individual results vary significantly based on production, client retention, expenses, and business model chosen.

Q: What is RIA advisor compensation in 2025?

A: RIA advisor compensation depends on whether advisors are solo or affiliated with a support platform:

Solo RIA advisors retain 100% of gross revenue but pay all operating expenses(technology, compliance, staff, office, insurance, etc.)

Affiliated RIA advisors share a percentage of revenue with their support platform in exchange for comprehensive back-office services

The key is determining which model provides the best net outcome after considering both financial returns and quality of life factors. Some advisors prefer complete independence despite higher operational burden; others value the support and time savings of affiliation.

Q: Do independent advisors make more than wirehouse advisors?

A: Many independent advisors report earning higher net income than wirehouse advisor sat comparable production levels, primarily due to:

- Higher payout structures (less corporate overhead)

- Elimination of various deductions and adjustments

- Ability to build equity value (wirehouses build $0)

However, individual results vary significantly based on:

● Production level

● Operational efficiency

● Client retention

● Business model chosen

● Expense management

Some advisors may earn less during transition periods or if they cannot successfully manage the operational complexity of independence. The economics are generally more favorable for independent advisors, but execution matters.

Q: What percentage of revenue do independent advisors keep?

A: Net retention varies significantly by model commonly referenced in industry literature:

● Solo RIA advisors: 100% gross minus 35-45% operating expenses = 55-65% net

● IBD-affiliated advisors: 80-90% gross minus 15-25% personal expenses = 65-75% net

● Hybrid RIA advisors: 90-95% gross minus 10-20% personal expenses = 70-85% net

● Employee advisors: 40-70% after grid, deductions, and adjustments

The key is comparing net take-home after ALL expenses, not just gross payout percentages. An advisor keeping 60% of production with comprehensive support may net more than an advisor keeping 100% but spending 20 hours weekly on operations.

Q: How does recurring revenue percentage affect advisor income?

A: Recurring revenue percentage dramatically impacts both income stability and practice valuation:

Income Stability:

● Low recurring (30%): High month-to-month variance, constant sales pressure

● High recurring (90%+): Predictable income, compounding growth

Practice Valuation:

● Low recurring: Lower valuation multiples (1.8-2.2x revenue)

● High recurring: Higher valuation multiples (2.5-3.5x+ revenue)

Business Model:

● Low recurring: Commission-driven, product conflicts, starting over each month

● High recurring: Fee-only, client alignment, sustainable growth

At Axiom according to internal documentation, advisors average approximately 97% recurring revenue (compared to industry averages of 30-35%), creating more stable businesses with higher valuations and better client alignment.

Evaluating Your Personal Income Potential

When considering independence, advisors should evaluate:

Your Current Situation:

● Production level

● Net take-home (after ALL deductions)

● Work hours per week

● Career satisfaction

● Equity value (typically $0 as employee)

● Recurring revenue percentage

● Time spent on operations vs. clients

Independent Potential:

● Expected production (often grows with better service)

● Expected net retention (varies by model)

● Expected work hours (typically decreases with support)

● Expected career satisfaction (typically increases)

● Expected equity building (varies by recurring revenue %)

● Expected operational burden (varies by model)

Key Questions to Ask:

- How much of my current income is recurring vs. transactional?

- What percentage of my time is spent on operations vs. clients?

- Am I building any equity value in my current position?

- Do I have product conflicts affecting my recommendations?

- What would my net income look like under different models?

Beyond Income: Total Life Value

In a verified interview, Bryan shared that his revenue rose from approximately $130,000 to over $300,000 in four years after transitioning. He described the move as the most impactful decision of his career. 'And the thing is, it’s not because I’m selling people stuff they don’t need. I’m helping people,' he said.

This is his personal experience and not typical. Individual results vary based on production, client retention, business model, and operational efficiency.

The transition to independence isn't just about income — it's about:

Professional Integrity: Serving clients without product conflicts or commission pressure

Work-Life Balance: Recurring revenue reduces constant prospecting pressure

Equity Building: Creating transferable business value for retirement or succession

Career Satisfaction: Alignment between personal values and daily actions

Client Relationships: Building authentic fiduciary relationships based on trust

Professional Pride: Feeling good about your work and recommendations

Take Your Next Step

Take Your Next Step Discover whether independence might be right for your practice with a complimentary, no-obligation consultation. We'll discuss:

● Your current situation and goals

● Different independence models available

● Transition process and timeline

● Support structures and resources

● Expected outcomes based on your specific circumstances This is a genuine exploration of your options, not a sales pitch.

Discover whether independence might be right for your practice with a complimentary, no-obligation consultation. We'll discuss:

● Your current situation and goals

● Different independence models available

● Transition process and timeline

● Support structures and resources

● Expected outcomes based on your specific circumstances

This is a genuine exploration of your options, not a sales pitch.

[Schedule Confidential Consultation]

Sources and References

Primary Sources (Verified from Project Files):

- Lane Team Member script - Internal interview conducted with Lane discussing his experience at Northwestern Mutual and transition to Axiom (2017-present). All quotes verified from recorded transcript.

- Bryan_Advisor_interview_Script - Recorded interview with Bryan discussing his 10-year experience at Northwestern Mutual ($100K income) and transition to Axiom (income grew to $300K+ within 4 years). All quotes verified from recorded transcript.

- Jerry_Zoom_Interview_Script - Recorded interview with Axiom founder discussing 97% recurring revenue model vs. 32% industry average, 95% advisor payout structure, and support model. All data points verified from recorded transcript.

- Axiom _ Comprehensive Macro Marketing Document pt1.docx - Internal document confirming 97% recurring revenue across organization, 95% payout structure, and business model details.

- Advisors_in_transition_research_ - Research findings about advisor attrition (80% of field recruits leave within first 5 years), reasons advisors leave (sales-driven culture, technology limitations, compensation issues, lack of entrepreneurial culture, fiduciary conflicts).

- Advisors_in_transition_research_ - Compiled research on pain points at various firms (Morgan Stanley, UBS, Wells Fargo, LPL, Raymond James, Commonwealth, Ameriprise, Northwestern Mutual, New York Life, MassMutual).

Industry Context

- FP Transitions - Referenced as industry source for practice valuation and transition services (https://www.fptransitions.com/)

Disclaimer

Income figures and testimonials presented represent specific individual experiences and are not guarantees of results. Bryan's reported income increase from $130,000 to $300,000 represents his individual outcome based on his specific circumstances, production, client base, and operational efficiency over a four-year period. Lane's experience represents his individual transition and outcomes.

Results vary significantly among advisors based on production level, recurring revenue percentage, operational efficiency, client retention, market conditions, individual capabilities, business model chosen, and numerous other factors. Past performance is not indicative of future results.

Illustrative examples provided in this article are for educational purposes only and do not represent guarantees, projections, or promises of specific income levels. Individual advisors should conduct their own analysis based on their specific circumstances.

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Advisors considering any career transition should conduct their own due diligence, consult with legal and financial professionals, and carefully evaluate their individual circumstances before making any decisions.

No compensation was provided for testimonials. All interview content used with permission and verified from recorded transcripts. Axiom Financial Partners is not making any representations or guarantees regarding income potential for prospective advisors.

Related Articles:

- Breaking Through the Solo Ceiling: A Guide to Building Enterprise-Level Advisory Firms

- Breaking Through the Hamster Wheel: The 5 Phases of Building a Sustainable Financial Advisory Practice

- How to Build a Never-Asking-For-Referrals Business