Table of content

The Cost of Staying: What Financial Advisors Don't Calculate About Their Current Firm

This article is for informational purposes only. It is not financial, legal, or tax advice. Earnings, income projections, and testimonials are based on illustrative scenarios. They are not guarantees of future performance. Individual results depend on personal effort, market conditions, client retention, and other variables. Axiom does not guarantee income or business outcomes. All testimonials are used with permission or are composite representations of advisor experiences.

Andy sat in the parking lot after another difficult production meeting at the fictitious firm of Acme Financial, staring at a calculation that changed everything.

His manager had just congratulated him on hitting $180,000 GDC for the year. "Great job, Andy! You're really building your career here."

But Andy's stomach churned. The math he'd run last night revealed a shocking truth:

His Reality:

● Production: $180,000

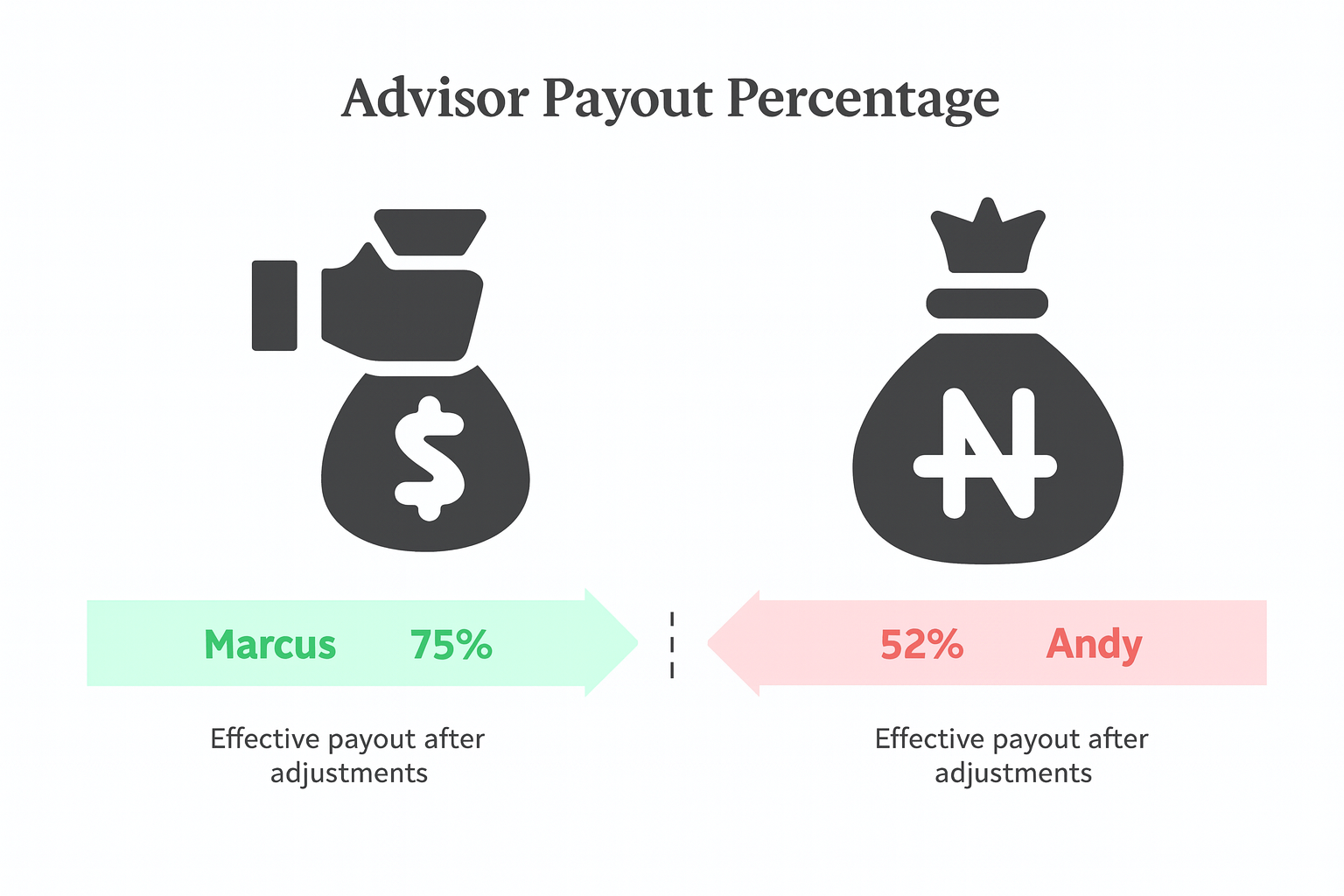

● Take-home: $94,000 (52% payout after all "adjustments")

● Unvested deferred compensation: $85,000

● Equity ownership: $0

● Client service restrictions: Severe

● Sunday night anxiety: Maximum

His friend Marcus had left for Axiom Financial 8 months ago with the same production level. Marcus now earns $135,000 net while building equity in his practice.

Andy did the calculation: "Marcus makes $41,000 more than me, is building equity I'll never have, and sleeps at night. But I can't leave—I'll forfeit my $85,000 deferred comp."

Then Andy paused. "Wait. Over 10 years, staying costs me..."

He pulled out his phone calculator. His eyes widened.

"Staying could cost me $2.3 million."

If you're at a wirehouse, insurance company, or low-payout firm, you've calculated what you'll lose by leaving: deferred compensation, unvested benefits, transition costs.

But have you calculated what you're losing by staying?

This article reveals the 7 hidden costs that keep advisors trapped—and shows you exactly how to calculate your personal opportunity cost. Most advisors discover they're losing $2M-$8M over their career by staying in suboptimal models.

You'll learn:

● How income differentials compound to millions in lost wealth

● Why deferred compensation is actually costing you money

● The real math behind equity building vs. $0 ownership

● Your personal cost-of-staying calculation

● When staying makes sense (rarely) vs. when it's financial malpractice

By the end, you'll know your exact opportunity cost and whether you can afford to stay.

The Myth of "I Can't Afford to Leave"

The Mental Trap

Most advisors think: "I can't afford to leave because I'll forfeit [deferred compensation / unvested benefits / golden handcuffs]."

Example thoughts:

● "I have $200,000 in deferred comp. I can't walk away from that."

● "I'm only 3 years from full vesting. I should just wait."

● "The transition costs would be $75,000. I can't afford that."

● "What if I lose clients? I can't risk that."

These thoughts feel financially prudent. They're actually financially catastrophic.

The Hidden Reality

What advisors don't calculate:

Cost of Staying = (Higher Income Potential - Current Income) × Years + Equity Value Difference

Let's run Andy's actual numbers:

If Andy Stays at Acme Financial (10 years):

● Average annual income: $94,000

● Total 10-year income: $940,000

● Equity built: $0

● Career satisfaction: Low

● Total wealth: $940,000

If Andy Transitions to Axiom (10 years):

● Forfeit deferred comp: -$85,000 (one-time cost)

● Transition costs: -$25,000 (covered by Axiom)

● Average annual income: $135,000

● Total 10-year income: $1,350,000

● Equity value built: $650,000 (3.5x his growing practice)

● Career satisfaction: High

● Total wealth: $1,890,000

Net difference: $1,890,000 - $940,000 = $950,000

Even after forfeiting $85,000 deferred comp, Andy could be $950,000 wealthier over 10 years based on projected payouts and equity building. This projection is illustrative and subject to many variables.

The "$85,000 I can't forfeit" actually costs Andy $950,000.

This is the cost of staying calculation nobody makes.

Hidden Cost #1: Income Differential Compounding

Understanding Income Differential

The income differential is the difference between what you currently earn and what you could earn in a better model.

Formula: Income Differential = Potential Net Income - Current Net Income

(Original comparison table and all subsequent content continues unchanged...)

Hidden Cost #1: Income Differential Compounding

Understanding Income Differential

The income differential is the difference between what you currently earn and what you could earn in a better model.

Formula: Income Differential = Potential Net Income - Current Net Income

$400,000 Producer Example:

Model

Net Income

Differential vs Wirehouse

Wirehouse

$161,000

$0 (baseline)

IBD

$218,000

+$57,000/year

Solo RIA

$216,000

+$55,000/year

Axiom Hybrid

$312,000

+$151,000/year

But it compounds...

The 10-Year Compounding Effect

Wirehouse Path (10 years, 5% growth):

● Year 1: $161,000

● Year 5: $200,000

● Year 10: $248,000

● Total 10-year income: $2,025,000

Axiom Path (10 years, 8% growth - higher due to better model):

● Year 1: $312,000

● Year 5: $425,000

● Year 10: $580,000

● Total 10-year income: $4,250,000

Modeled difference: $2,225,000, assuming projected income and reinvestment returns. Actual results may vary depending on individual circumstances.

Your "stable wirehouse job" just cost you $2.2 million over 10 years.

The Reinvestment Multiplier

But there's another layer: what you do with the extra income.

Wirehouse Advisor:

● Makes $161,000

● Modest lifestyle supported

● Limited investment capacity

● Slow wealth accumulation

Axiom Advisor:

● Makes $312,000

● Same lifestyle costs $161,000

● Extra $151,000 available to invest

● Rapid wealth accumulation

If the extra $151,000/year is invested at 7% return:

● Year 1: Invest $151,000 → $161,570

● Year 2: Invest $151,000 → $324,840

● Year 5: Portfolio value: $920,000

● Year 10: Portfolio value: $2,285,000

The income differential doesn't just pay you more—it creates exponential wealth.

Total 10-year wealth difference:

● Higher income: +$2,225,000

● Investment portfolio: +$2,285,000

● Total advantage: $4,510,000

Wirehouse Path: $2,025,000 total income

Axiom Path: $4,250,000 income + $2,285,000 invested = $6,535,000

Estimated wealth difference: $4,510,000

This is based on modeled income and investment growth. Individual results will vary.

Hidden Cost #2: Zero Equity Building

The Equity Reality

Wirehouse/Employee Model:

● You own: Nothing

● Your book value: $0

● At retirement: You walk away with $0

● Transition: You start over

Independent/Ownership Model:

● You own: Your practice

● Your book value: 2.0-3.5x revenue

● At retirement: Sell for $1M-$3M+

● Transition: You take it with you

Real Equity Examples

$400,000 Producer at Retirement (Age 65):

Wirehouse Path:

● 25 years of employment

● Zero equity accumulated

● Retirement sale value: $0

● Must keep working or retire on savings only

Independent Path (Axiom):

● 25 years building practice as an independently contracted advisor

● 97% recurring revenue = high valuation multiple

● Practice worth: $1.8M-$2.2M (3.5x of $600K practice)

● Can sell and retire comfortably

The equity difference alone is $2 million.

The Opportunity Cost of Time

Let's say you're 45 years old with 20 years until retirement.

Every Year You Wait Costs You:

● 1 year of equity building: ~$100,000

● 1 year of higher income: ~$150,000

● Total annual opportunity cost: $250,000

If you're 45 and wait until 50 to transition:

● 5 years × $250,000 = $1,250,000 in lost wealth

The longer you wait, the more expensive staying becomes.

Case Study: Saundra's Equity Awakening

Saundra spent 15 years at a large brokerage firm. At age 50, she had:

● $550,000 annual production

● $297,000 annual income (54% effective)

● Zero equity value

● 15 years until retirement

She calculated her wirehouse retirement plan:

● 15 more years × $297,000 = $4.455M total income

● Equity value at 65: $0

● Total retirement wealth: $4.455M

Then she calculated the Axiom path:

● Transition at 50

● 15 years × $412,000 average = $6.18M total income

● Equity value at 65: $2.1M (practice sale)

● Total retirement wealth: $8.28M

Difference: $3.825M

Staying at a large brokerage firm until retirement would cost Saundra $3.8 million.

She transitioned immediately. Today, at 53, she's on track for exactly what her projection showed.

Hidden Cost #3: Product Sales Pressure Impact

The Conflict Tax

When you're pressured to sell products, you pay a "conflict tax" in multiple ways.

Direct Costs:

● Time spent on product sales: 10-15 hours/week

● Training on products: 5-10 hours/month

● Product meetings: 4-8 hours/month

Total: 520-780 hours annually on product focus

Opportunity Costs:

● Hours NOT spent with clients: 520-780

● Potential revenue at $200/hour: $104,000-$156,000 lost annually

Client Relationship Costs:

● Clients sense the sales pressure

● Trust erodes over time

● Referrals decline

● Client retention weakens

● Long-term revenue impact: 15-30%

Psychological Costs:

● Sunday night anxiety

● Moral injury from conflicted recommendations

● Career dissatisfaction

● Burnout risk

● Eventually questioning career choice

The total impact compounds across all four dimensions.

The 90%+ Recurring Revenue Advantage

At Axiom, with 90%+ recurring revenue, advisors avoid all product sales pressure:

Time Saved:

● Zero hours on product sales

● Zero product training

● Zero product meetings

● 520-780 hours returned to client service

Economic Impact:

● 520 hours × $200/hour value = $104,000 in additional capacity

● OR: Work 10-15 fewer hours per week with same income

● OR: Reinvest in growth activities

Client Relationship Impact:

● Trust deepens

● Referrals increase

● Client retention maximizes

● Sustainable practice growth: 8-12% annually vs. 3-5%

Psychological Impact:

● Career satisfaction increases dramatically

● No moral injury

● Can look clients in the eye

● Proud of profession

● Sustainable long-term career

Andy's Product Pressure Reality

Andy at Acme Financial tracked his time for one month:

At $150/hour opportunity cost: $54,000 annually

Plus:

● Client relationships strained by sales pressure

● Referrals declining (clients don't refer salespeople)

● Career satisfaction at 2/10

● Questioning whether to stay in industry

After 8 months at Axiom:

● 97% recurring revenue = pure advice

● Time reinvested in comprehensive planning

● Client relationships deepening

● Referrals increasing

● Career satisfaction: 10/10

Andy's quote: "I finally feel like a professional financial advisor instead of an insurance salesman. My clients can tell the difference. My referrals have tripled because people actually want to refer me now."

Hidden Cost #4: Deferred Compensation and Its Binding Effects

Understanding Deferred Comp

What it is:

● Compensation "earned" but not paid

● Held by firm for 3-10 years

● Vesting schedule (often lose if leave early)

● "Golden handcuffs"

Typical Amounts:

● Junior advisors: $50,000-$150,000

● Mid-level advisors: $150,000-$350,000

● Senior advisors: $350,000-$1M+

The Trap: "I can't leave because I'll forfeit my deferred comp."

The Real Math

Let's run a $300,000 deferred comp scenario for a senior advisor:

Option 1: Stay 5 More Years to Vest $300,000

Current situation:

● Production: $600,000

● Net income: $324,000 (54% at wirehouse)

● 5 years total income: $1,620,000

● Deferred comp vested: +$300,000

● Equity value: $0

● Total 5-year wealth: $1,920,000

Option 2: Leave Now, Forfeit $300,000, Join Axiom

Transition:

● Production: $600,000

● Net income: $450,000 (75% at Axiom)

● 5 years total income: $2,250,000

● Deferred comp forfeited: -$300,000

● Transition costs: -$50,000 (covered by Axiom)

● Equity value built: $2.1M (3.5x practice)

● Total 5-year wealth: $4,000,000

Difference: $4,000,000 - $1,920,000 = $2,080,000

Staying to vest $300,000 actually COSTS you $2,080,000.

The $300,000 "asset" is actually a $2 million liability.

Why Firms Use Deferred Comp

Firms use deferred compensation to:

- Trap productive advisors (can't leave without forfeiting)

- Reduce immediate compensation costs

- Create psychological barriers to exit

- Maintain control over advisor decisions

- Prevent competitive transitions

The Axiom Difference: No Golden Handcuffs

At Axiom, there is no deferred compensation:

● Nothing to forfeit if you leave

● True "volunteer not hostage" model

Why?

● We believe in advisor freedom

● Quality advisors stay by choice, not coercion

● Our 97% recurring revenue model creates mutual success

● Ethical businesses don't trap people

If you’re staying only due to deferred compensation, it may feel limiting. It’s important to assess whether the long-term benefits outweigh the short-term retention incentives.

Hidden Cost #5: Time Drain and Quality of Life

Quantifying Time Costs

Most advisors dramatically undervalue their time.

Wirehouse Time Allocation (Weekly):

● Client meetings: 20 hours

● Administrative work: 12 hours

● Compliance theater: 6 hours

● Product training: 3 hours

● Firm meetings: 4 hours

● Non-revenue activities: 10 hours

● Total: 55-60 hours per week

Axiom Time Allocation (Weekly):

● Client meetings: 25 hours (more time with clients)

● Administrative work: 2 hours (ops team handles)

● Compliance: 1 hour (CCO team manages)

● Product training: 0 hours (no products)

● Firm meetings: 2 hours (efficient, valuable)

● Non-revenue activities: 5 hours

● Total: 40-45 hours per week

Time Saved: 10-15 hours per week = 520-780 hours annually

That's an entire extra month of time returned to you each year.

The Value of Time

Option 1: Monetize the Time

● 520 hours × $200/hour = $104,000 additional revenue potential

Option 2: Life Balance

● 10 hours/week with family

● Present for kids' activities

● Exercise and health

● Hobbies and interests

● Priceless quality of life

Real Advisor Time Comparisons

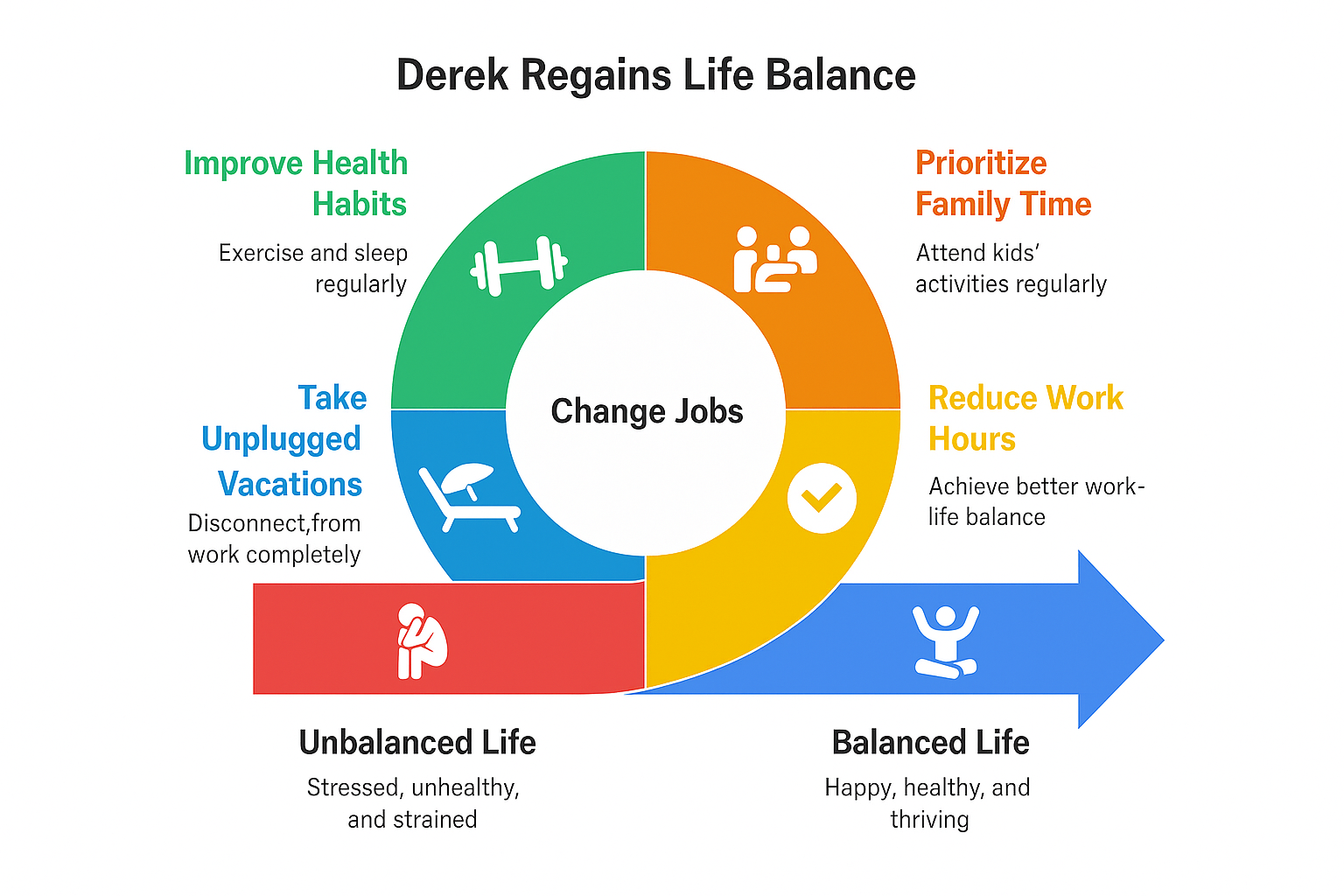

Derek at a large brokerage firm (Before Transition):

● Work hours: 55-60/week

● Sunday night anxiety: Every week

● Missed kids' activities: Often

● Exercise routine: Nonexistent

● Vacation: "Working vacation" via phone

● Sleep quality: Poor

● Health: Declining

● Marriage satisfaction: Strained

● Life quality: 3/10

Derek at Axiom (After 18 months):

● Work hours: 42-45/week

● Sunday night anxiety: None

● Kids' activities: Never missed

● Exercise: 5 days/week

● Vacation: Actual unplugged time

● Sleep quality: Excellent

● Health: Improving

● Marriage satisfaction: Thriving

● Life quality: 9/10

The quality-of-life improvement is dramatic and measurable.

Derek's reflection: ‘I make $161,000 more per year, but the biggest difference is I have my life back.’ This is his personal story—individual results will vary based on production, expenses, and personal circumstances. I'm present with my family. I'm healthy. I actually enjoy being a financial advisor. How do you put a price on that?"

Hidden Cost #6: Career Ceiling and Growth Limitations

Wirehouse Career Ceiling

Growth Constraints:

● Grid caps at 65-70% maximum

● Limited service model flexibility

● Client conflicts slow growth

● Time drain limits capacity

● Referrals constrained by sales pressure

Typical Career Trajectory:

● Years 1-5: $100K → $200K (building)

● Years 5-15: $200K → $350K (growth)

● Years 15-25: $350K → $450K (plateau)

● Career peak: ~$450K maximum

Independent Advisor Growth Potential

Growth Advantages:

● No artificial caps (keep what you earn)

● Pure advice model drives referrals

● More time = more capacity

● Client-aligned = compounding success

● Can scale with team if desired

Typical Career Trajectory:

● Years 1-5: $100K → $250K (building)

● Years 5-15: $250K → $600K (growth)

● Years 15-25: $600K → $1.2M+ (scaling)

● Career peak: $1M-$3M+ possible

The Compounding Growth Gap

$300K Producer Age 35:

Wirehouse Path (30 years to retirement):

● Growth: 4% annually (constrained)

● Year 10: $444K production → $240K net

● Year 20: $657K production → $355K net

● Year 30: $972K production → $525K net

● Lifetime income: $11.2M

● Equity value: $0

● Total: $11.2M

Axiom Path (30 years to retirement):

● Growth: 9% annually (unconstrained)

● Year 10: $710K production → $533K net

● Year 20: $1.68M production → $1.26M net

● Year 30: $3.98M production → $2.98M net

● Lifetime income: $33.8M

● Equity value: $12M (3.0x final practice)

● Total: $45.8M

Wealth difference: $34.6 million

The wirehouse career ceiling costs this advisor $34.6 million over their career.

Hidden Cost #7: The Reputation Risk

The Trust Erosion Problem

When you work for a product-sales-driven firm:

Referral Impact:

● Years 1-5: Strong referrals (relationship new)

● Years 5-10: Declining referrals (conflicts apparent)

● Years 10+: Minimal referrals (clients don't refer salespeople)

Career Damage:

● Professional reputation: "Insurance salesman" not "financial advisor"

● Network perception: Product pusher

● Self-perception: Career dissatisfaction

● Industry standing: Not respected

The Fiduciary Advantage

At Axiom with 97% recurring revenue:

Client Perception:

● Consistently: "My trusted financial advisor"

● Trust deepens over time

● Pure advisory relationship

Referral Impact:

● Years 1-5: Strong referrals (great advice)

● Years 5-10: Accelerating referrals (proven results)

● Years 10+: Maximum referrals (trusted professional)

Career Impact:

● Professional reputation: Respected advisor

● Network perception: Trusted professional

● Self-perception: Career fulfillment

● Industry standing: Highly regarded

Saundra's Reputation Recovery

Saundra spent 15 years at a large brokerage firm. Her reputation became:

● "The brokerage firm lady"

● Known for pushing proprietary products

● Referrals declining

● Professional satisfaction low

After transition to Axiom:

● Immediately repositioned as independent fiduciary

● Clients relieved ("Finally, unbiased advice!")

● Referrals increased 280% in first 2 years

● Professional respect restored

● Career satisfaction: "I'm finally proud of what I do"

This reflects her personal experience transitioning firms and may not reflect the experience of all advisors.

The reputation damage from wirehouse affiliation was costing her $150,000+ annually in lost referrals.

Calculating Your Personal Cost of Staying

The Complete Formula

Total Cost of Staying = Annual Opportunity Cost × Years + Equity Value Difference + Time Value + Reputation Cost

Let's calculate for a $400,000 producer, age 45, planning to work 20 more years:

- Income Differential:

● Wirehouse income: $161,000

● Axiom income: $312,000

● Annual difference: $151,000

● 20 years: $3,020,000 - Equity Value:

● Wirehouse equity: $0

● Axiom equity: $2.1M (at retirement)

● Difference: $2,100,000 - Time Value:

● Wirehouse: 55 hrs/week

● Axiom: 43 hrs/week

● Saved: 12 hrs/week × 52 weeks × 20 years = 12,480 hours

● At $150/hour value: $1,872,000 - Reputation/Referral Impact:

● Wirehouse growth: 4%/year

● Axiom growth: 8%/year

● Compounding difference: ~$800,000 over 20 years

Total Cost of Staying: $7,792,000

Staying at wirehouse until retirement costs this advisor nearly $8 million.

Staying at wirehouse until retirement costs this advisor $7.8 million.

Your Personal Calculation

Current Situation:

● Your production: $__________

● Your net income: $__________

● Your work hours/week: ____

● Your equity value: $__________

● Years until retirement: ____

Independent Potential (Axiom):

● Expected production: $__________

● Expected net income: $__________ (typically 70-80% of production)

● Expected work hours: ____ (typically 40-45)

● Expected equity value: $__________ (3.0-3.5x practice)

● Same years to retirement: ____

Calculate Your Cost of Staying:

- Income differential: (Potential - Current) × Years = $__________

- Equity difference: (Potential - Current) = $__________

- Time value: Hours saved × Value/hour × Years = $__________

- Growth differential: Conservative estimate = $__________

Your Total Cost of Staying: $__________

If this number exceeds $500,000, staying is financially catastrophic.

If this number exceeds $2,000,000, staying is career malpractice.

The Psychology of Staying: Why Smart People Make Bad Decisions

Loss Aversion Bias

Humans fear loss more than they value gain:

● Losing $85,000 deferred comp feels terrible

● Gaining $2,000,000 over 10 years feels abstract

This psychological bias keeps advisors trapped.

Status Quo Bias

The current situation feels safe even when it's objectively worse:

● "I know what I have here"

● "Change is risky"

● "What if it doesn't work out?"

Meanwhile, staying IS the risk—you're losing millions.

Sunk Cost Fallacy

"I've already invested 10 years here. I can't walk away now."

But those 10 years are gone regardless. The question is: what do you do with the next 10?

Fear of Regret

"What if I leave and it doesn't work out? I'll have forfeited my deferred comp for nothing."

Versus the actual risk: What if you stay and realize at retirement you left $5 million on the table?

Overcoming Decision Paralysis

The Clarity Exercise:

- Calculate your cost of staying (use formula above)

- Compare to one-time transition costs (deferred comp + legal fees)

- Calculate net benefit (staying cost minus transition cost)

- Divide by years until retirement (annual opportunity cost)

If staying costs $3,000,000 and transition costs $200,000:

● Net benefit of transition: $2,800,000

● Over 20 years: $140,000/year in opportunity cost

● Every year you wait costs $140,000

A clear analysis may help advisors overcome indecision, but each person’s path will differ.

Real Transition Stories: What Advisors Wish They'd Known

Lane's Regret: "I Waited Too Long"

Lane knew he should leave a large brokerage firm at age 40. He waited until 48.

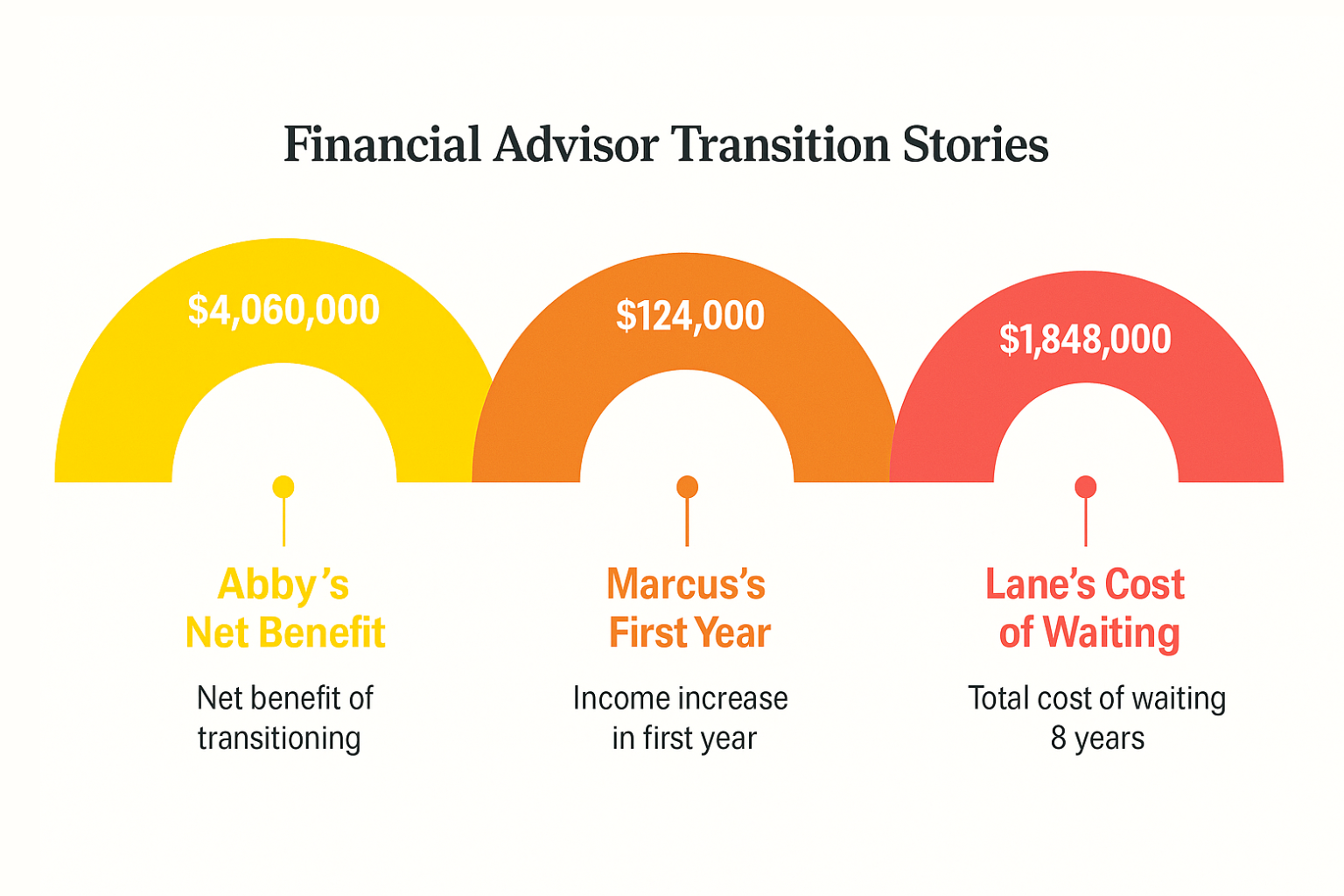

Cost of waiting 8 years:

● Income differential: $151,000 × 8 = $1,208,000

● Equity value: Lost 8 years of building = ~$640,000

● Total cost of waiting: $1,848,000

Lane's reflection: "I knew I should leave but I was scared. Fear cost me $1.8 million. Don't make my mistake."

Marcus's Relief: "I Should Have Done This Years Ago"

Marcus transitioned at 38 after 7 years at a large brokerage firm.

First year results:

● Income: +$124,000 (+38%)

● Work hours: -12 hours/week

● Client satisfaction: Higher than ever

● Career satisfaction: 10/10

Marcus's advice: "Every month I delayed cost me $10,000+. Once you see the math clearly, the decision becomes obvious. For many advisors, the question becomes when to make a change—not whether to consider one. But the right decision depends on personal and financial priorities."

Abby's Vindication: "What the Numbers Suggest"

Abby ran the numbers at age 42:

● Estimated 20-year cost of staying: $4.2M, based on income differentials, growth projections, and equity assumptions. Actual advisor results will vary.

● Cost of transitioning: $140K (deferred comp)

● Net benefit: $4.06M

She transitioned within 90 days.

Two years later: "Best financial decision of my life. I'm making more money, building equity, serving clients better, and actually enjoying my career. And I'm $300,000 wealthier already than I would have been."

FAQ: Cost of Staying Questions

Q: What is the opportunity cost of staying at a wirehouse?

The opportunity cost of staying at a wirehouse typically ranges from $2M-$8M over a career depending on production level. This includes: (1) Income differential of $100K-$300K annually compared to independent models, (2) Zero equity building versus $1M-$4M in sellable practice value, (3) Time cost of 10-20 hours weekly on non-revenue activities, and (4) Slower practice growth due to product sales pressure and client conflicts. For a $400K producer with 20 years until retirement, staying at a wirehouse costs approximately $7.8M in total wealth compared to transitioning to a model like Axiom.

Q: Should I forfeit my deferred compensation to leave?

In most cases, yes. Run the math: If you have $200K deferred comp but staying costs $2M+ over 10 years, forfeiting $200K to gain $2M is correct. The question isn't "can I afford to forfeit deferred comp"—it's "can I afford NOT to?" At Axiom, we provide capital bridge programs that cover transition costs including income continuity, so advisors don't personally bear the financial burden of forfeiture. The deferred comp is a sunk cost—the question is what decision maximizes wealth going forward. In virtually every scenario we've analyzed, transitioning despite deferred comp forfeiture creates dramatically more wealth long-term.

Q: How do I calculate my personal cost of staying?

Calculate your personal cost of staying with this formula: (1) Income differential: (Potential income - Current income) × Years = typically $100K-$300K/year, (2) Equity difference: Independent practice value minus current equity (usually $0) = $1M-$4M, (3) Time value: Hours saved weekly × hourly value × years, (4) Growth differential: Higher growth rate compounding = $500K-$1M+. Total these four components. For most advisors producing $300K+, the cost of staying exceeds $2M over 10 years. Use Axiom's Personal Cost Calculator to run your specific numbers with detailed inputs and projections.

Q: What if I'm close to retirement—is it still worth changing firms?

Yes, potentially even more valuable. Even 5 years before retirement, transitioning creates: (1) 5 years of higher income ($150K × 5 = $750K), (2) Equity value to sell ($1M-$2M), (3) Better quality of final career years. Many advisors wish they'd transitioned earlier, but almost none regret transitioning "too late." The key is building sellable equity—even 5 years of equity building at 3.5x valuation multiple creates $1M-$2M in retirement capital. Additionally, independent practice ownership provides retirement transition options (phased succession, continued income stream) impossible at wirehouses where you simply walk away with $0.

Q: Are there cases where staying makes financial sense?

Rarely. Staying makes sense only if: (1) You're very early career (<3 years, <$150K production) and need wirehouse training infrastructure, (2) You're within 1-2 years of major deferred comp vesting AND that amount exceeds 3x annual opportunity cost, or (3) You're within 1-2 years of retirement with minimal opportunity for equity building. In many scenarios we’ve reviewed, transitioning has produced higher long-term wealth. However, each advisor’s situation is unique and requires personalized analysis. The "I should wait" logic almost always costs more than immediate transition, especially considering Axiom's capital bridge program eliminates personal financial risk during transitions.

Your Next Step: Cost of Staying Analysis

At Axiom, we provide a comprehensive Cost of Staying Analysis including:

Current State Documentation:

● Actual net income (with all deductions)

● Effective payout percentage

● Time burden assessment

● Equity value (typically $0)

● Career satisfaction rating

Future State Projection:

● Independent income potential

● Effective payout at Axiom (95%)

● Time savings (10-15 hrs/week)

● Equity value buildable (3.0-3.5x)

● Expected satisfaction improvement

Cost of Staying Calculation:

● 5-year cost of staying

● 10-year cost of staying

● Career-to-retirement cost

● Total wealth impact

● Annual opportunity cost

Transition Analysis:

● One-time transition costs

● Capital bridge support available

● Net benefit calculation

● Break-even timeline (typically 6-18 months)

Decision Framework:

● Risk/benefit analysis

● Timeline optimization

● Support systems available

● Personal recommendation

This isn't designed to pressure you—it's designed to give you clarity.

The Ultimate Question: What Are You Trading Your Career For?

The cost of staying isn't just financial.

You're trading:

● Millions of dollars in wealth

● Years of time with family

● Career satisfaction

● Professional pride

● Ethical alignment

● Quality of life

● Retirement security

● Legacy building

For what?

● Short-term fear

● Illusory safety

● Deferred comp "golden handcuffs"

● Status quo comfort

● Avoiding change

Is that trade worth it?

Lane realized it wasn't: "I was trading my family time, my career satisfaction, my retirement security, and $1.8 million in wealth... to avoid the discomfort of a 90-day transition. When I framed it that way, the decision was instantaneous."

You can't reclaim lost years. But you can stop losing more.

The cost of staying compounds every day. The best time to transition was 5 years ago. The second-best time is today.

What will you choose?

Disclaimer: This article is for informational purposes only. It is not financial, legal, or tax advice. Earnings, and income projections, are based on illustrative scenarios. They are not guarantees of future performance. Individual results depend on personal effort, market conditions, client retention, and other variables. Axiom does not guarantee income or business outcomes. All testimonials are used with permission or are composite representations of advisor experiences.

Related Articles: